Global banks must run identity and credit checks under local rules. Barclays Credit Card applications follow that pattern across markets, with small differences between the United Kingdom and the United States.

Preparation speeds decisions, avoids repeat documentation requests, and prevents accidental score dents.

Who Issues Barclays Credit Cards In Different Countries

Barclays runs consumer cards in several markets through local entities. In the United Kingdom, cards are issued by Barclaycard under the broader Barclays UK brand.

In the United States, most consumer cards are co-branded and issued by Barclays Bank Delaware, also known as Barclays US Consumer Bank.

Regional product names, disclosures, and onboarding flows vary, yet the backbone stays the same:

- identity verification,

- affordability checks, and a

- credit bureau review.

Eligibility Basics and Credit Checks

Card issuers assess affordability and risk before opening a revolving credit line. United Kingdom applicants get decisions under conduct rules overseen by the Financial Conduct Authority, including creditworthiness guidance and clear “Representative APR” disclosures.

United States applicants fall under the Consumer Financial Protection Bureau and the Fair Credit Reporting Act.

Expect a soft search when using a pre-check tool and a hard inquiry at full submission. Credit files are typically pulled from Experian, Equifax, or TransUnion, depending on the country and program.

Documents To Prepare

Clear scans and consistent data shorten onboarding and reduce the number of referrals that go to manual review.

- Government ID that matches application details, for example, a passport or national ID.

- Proof of address dated within the last three months, such as a utility bill or bank statement.

- Proof of income was requested, including payslips or tax forms that show regular deposits.

- Existing bank details for identity cross-checks and potential direct debit setup.

- Loyalty numbers for co-branded cards when rewards programs are linked at account opening.

How To Apply For A Barclays Credit Card Online

Efficient applications follow a short, predictable flow that keeps data consistent across forms.

- Start with the Barclays eligibility checker or US pre-qualification to gauge likely approval.

- Complete the application using identical identity details to those on your documents.

- Provide income and housing information accurately, including bonuses only if reliably received.

- Consent to a credit check and submit; expect an instant decision or a short pending review.

- Respond quickly to verification requests, then activate the card and set controls in the app.

What Happens After Submission

Many applications receive quick outcomes through automated underwriting models. Some are referred for manual review when credit files show thin history, recent moves, or mismatched addresses.

A pending status may trigger a quick identity call or a document upload request. After approval, expect a physical card delivery window that depends on the issuing country and postal timelines.

Activation flows usually include PIN setup for UK cards and app enrollment for US cards. Spend controls, notifications, and travel alerts can be configured immediately inside the mobile app.

Barclays Eligibility Checker and Pre-Approval

United Kingdom applicants can use the Barclays eligibility checker powered by a soft search that leaves no footprint visible to lenders.

This tool estimates acceptance odds across selected Barclaycard products without committing to a hard inquiry.

United States applicants typically see a “See if you pre-qualify” option for several co-branded cards; the result indicates likelihood, not a guarantee. Soft searches help time applications and avoid stacking multiple hard inquiries in a short period.

APR, Fees, and Promotional Offers

Pricing is product-specific and adjusts by market, risk band, and promotional cycle. United Kingdom marketing includes a Representative APR that signals typical pricing for most accepted applicants, alongside balance transfer or purchase offers with clear end dates and fees.

United States disclosures use the Schumer box to present variable APR ranges, annual fees where applicable, balance transfer fees, cash advance fees, and foreign transaction fees.

Promotional rates can change after the intro period, so plan repayments against the standard purchase APR to avoid surprises.

Improving Approval Odds

Underwriters reward clean files, stable income, and consistent identity data.

- Lower credit utilization below common thresholds before applying, ideally below 30%.

- Fix errors on your credit report through the relevant bureau’s dispute process ahead of time.

- Avoid multiple hard inquiries in the weeks leading up to the application date.

- Keep addresses and employer details aligned across banking, payroll, and credit files.

- Add established accounts to your credit profile if thin history is an issue, where allowed.

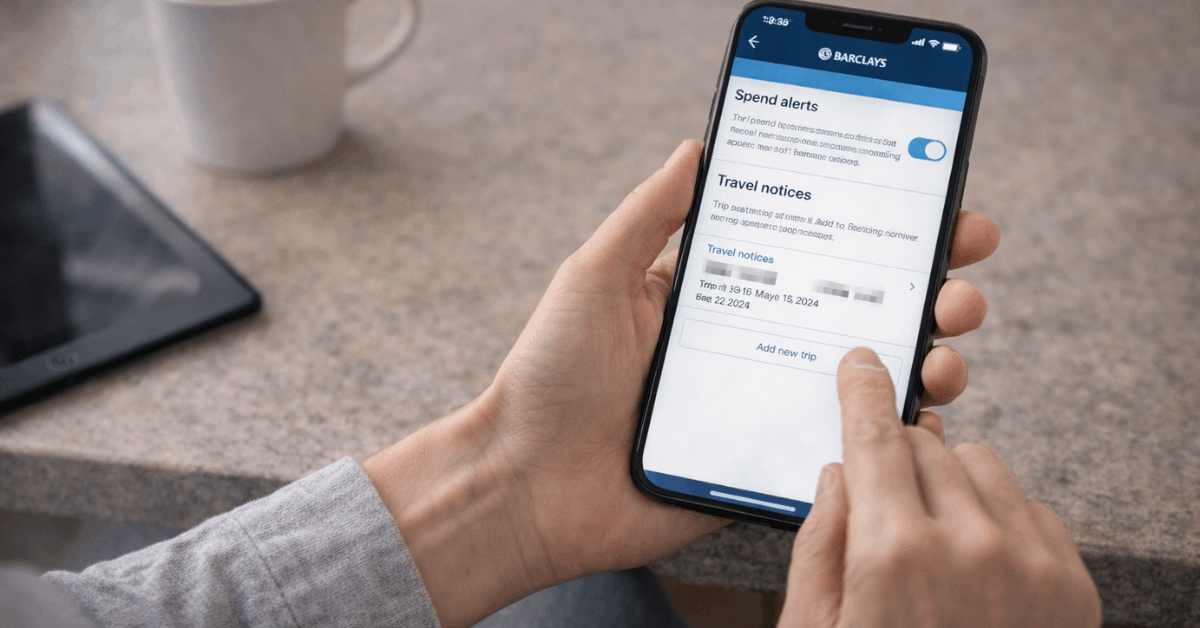

Security, Verification, and Account Setup

Identity verification aligns with anti-money-laundering rules and local KYC requirements. Document scans should be legible, uncropped, and free of glare. App setup is worth doing on day one because spend alerts and location-based controls can stop fraud quickly.

Contactless limits, travel notices, and card-not-present settings live inside the Barclays Mobile App. Two-factor authentication protects online access, while 3-D Secure prompts may appear during e-commerce checkouts depending on merchant risk signals.

Country Notes: UK and the United States

Strong candidates adapt to local mechanics while following the same preparation checklist. The table highlights practical differences that commonly affect timing and expectations.

Regional rules shape disclosures, credit bureau pulls, and activation steps. UK applicants see Representative APRs and PIN setup norms.

US applicants navigate co-branded lineups and variable APR ranges. Pre-checks are soft searches in both regions, yet final decisions always rely on a hard inquiry.

| Topic | United Kingdom | United States |

| Issuer entity | Barclaycard under Barclays UK | Barclays Bank Delaware |

| Pre-check tool | Barclays eligibility checker using soft search | Barclays pre-qualification using soft inquiry |

| Residency basics | Typically UK resident aged 18 or over | US resident with SSN or ITIN, age 18 or over |

| Typical bureaus | Experian, Equifax, TransUnion | TransUnion, Equifax, Experian |

| Activation setup | PIN and app controls | App controls and online access setup |

Common Mistakes To Avoid

Rushing an application often leads to mismatched addresses or inflated income figures that fail verification.

Submitting partial scans or screenshots can stall KYC because text fails automated checks. Applying during a stretch of new credit lines can depress acceptance odds by signaling elevated risk.

Ignoring the end date on a balance transfer offer leads to surprise interest once the promotional period lapses. Skipping app controls removes useful guardrails that prevent card-not-present fraud on day one.

Conclusion

A clean file and consistent documents put you in the fastest lane. Use the Barclays eligibility checker first, then submit accurate details and respond quickly to any verification.

Plan repayments around standard APRs, not temporary offers, and avoid back-to-back applications. Once approved, activate the card, enable app controls, and keep address and income data aligned.

Note: This site provides general information on credit cards and payment products, not financial, legal, or tax advice; always verify rates, fees, and terms with the issuing bank before applying.